ACCA’s Digital Horizons report reflects on how accountants see the role technology will play in their future

Financial professionals share a sense of optimism about digital transformation including AI (artificial intelligence).

A survey among members of ACCA (the Association of Chartered Certified Accountants) sees a range of key organisational benefits in adopting digital technologies, including flexibility/adaptability, and quality of products and services (78%); and sustainability performance, transparency and regulatory compliance (72%).

However, The Digital Horizons survey – which garnered 1,074 responses from ACCA members across the globe – noted that financial professionals still see the main benefit of technology as offering efficiency/process improvements (52%), with efficiency, internal process optimisation or cost savings ranked in their top three objectives when adopting a new technology.

Only 18% included competition-related reasons, such as responding to customer demands, enhancing market insights, introducing 24/7 capabilities, or maintaining competitive advantage.

Cost remains the top challenge when adopting technology, but organisational culture also remains a critical factor in successful adoption.

Andrew Lim, Portfolio Head, ACCA Maritime Southeast Asia said: ‘Successful technology adoption is not just about implementing new systems but also about enabling people to use these systems effectively and to realise their personal benefits. Hands-on experience and training are important, and so is the ability to experiment and innovate to improve existing task loads.

‘There is no panacea to improved adoption. While having the right objectives, skills and leadership are crucial, these factors do not stand alone. They must be connected within an overarching strategic vision that clearly prioritises as well as connects internal efficiency gains with more competitive and potentially transformative goals.’

The Digital Horizons report underlines the idea that the finance profession is well-situated to benefit from digital technologies but realising their potential could require a mindset shift – thinking beyond mere efficiency gains towards a deeper understanding of value – as well as an adaptation of skills and practices.

The survey did see a more mixed response to how technology supports personal objectives. Productivity (cited by 85% of respondents), collaboration (76%) and career development (65%) were all strong, while job security was less apparent, with only 30% saying technology was supportive in that respect. The impact on career development was notably positive, with many roundtable discussions revolving around access to learning and more flexible opportunities.

Lim said: ‘A key strategic advantage of automation in accounting is the shift from reactive to proactive accounting. With automation, accountants can focus more closely on analysing data and providing strategic insights rather than merely recording transactions.’

He added: ‘As technology evolves, it is important to think beyond efficiency because the acceleration of business will also amplify demands on the finance department. It might be necessary to reconstruct tasks to genuinely harness technology as an enabler of human capabilities and a converter of value.’

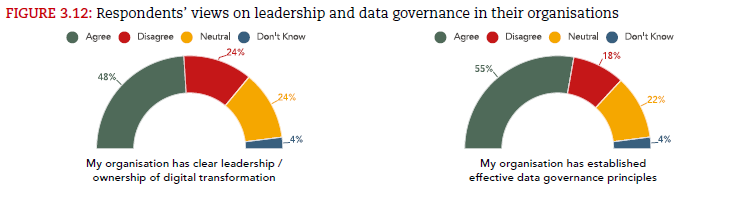

Leadership emerged as a key theme in both the survey and the roundtables.

Alistair Brisbourne, head of technology research ACCA, said: ‘Leadership is generally considered to be a cornerstone of successful innovation and yet it can seem quite vague as a concept when applied to digital transformation. At its core, embracing digital leadership means fostering a culture of innovation, encouraging continuous learning and being open to change.

‘When we analyse the findings, it is clear that leadership is a fundamental trait of the most innovative organisations, and this tends to coincide with greater individual confidence amongst employees. Digital leaders inspire the confidence to embrace new tools and methodologies, such as AI and advanced analytics, which can dramatically transform processes.’

The survey found ACCA members have a high level of trust in artificial intelligence (AI), with 70% of all respondents agreeing with the statement ‘AI can increase the amount of time I have to focus on business-critical tasks’; only 9% disagreed, while 15% were neutral. They were less sure of the idea of AI performing business-critical tasks (50% agreeing, 21% disagreeing and 22% neutral). Even so, the numbers still reflected a sense of optimism.

Although just under one-fifth report the implementation of AI within their organisation, and another 8% are trialling initiatives, there are clearly great aspirations and a considerable opportunity to leverage these new capabilities.

Brisbourne said: ‘To a significant extent, AI is still thought about in terms of a gradual evolution of existing processes. From this perspective, the potential of AI is primarily in making the industry more efficient rather than thinking about how it could be fundamental to driving value related to new and existing demands.’

Basic AI literacy is key. Finance professionals must understand the capabilities, limitations and potential applications of AI within their specific domains. Marrying technical skill sets with strategic understanding will be essential to harness the true potential of technologies such as AI.

Lim said: ‘The adoption of AI increases rather than decreases the importance of experts – such as finance and/or risk professionals – to oversee critical processes and functions.

He added: ‘AI may offer helpful support and productivity boosts, but it will not be able to replace the ability to think critically and take into account a broad array of contextual factors when making decisions, even when made on the basis of AI-driven insights.’

![[Photo] Andrew Lim_Portfolio Head, ACCA Maritime Southeast Asia](https://hrhub.my/wp-content/uploads/2023/11/Photo-Andrew-Lim_Portfolio-Head-ACCA-Maritime-Southeast-Asia.jpg)

.jpg)

.jpg)

{kind=link}